We're all Special Situations Funds Now

Observing (and marking) venture portfolios honestly—and an analogy to Japan's Lost Decades

Yesterday, Institutional Investor’s headline article was “More Pain to Come in PE, VC” with NEPC’s Sarah Samuels explaining that not only have investors not been getting distributions, but “many VC firms are keeping the valuations of holdings at 2021 and 2022 levels, which were peak years for the market,” and expecting more down marks eventually.

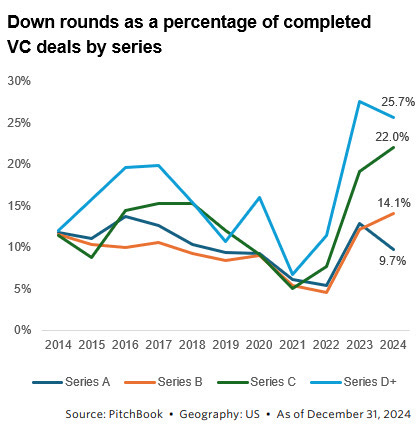

Similarly gloomy, last week’s Pitchbook newsletter led with, “Record highs for down rounds” with 2024 setting decade highs for down rounds, especially in late-stage companies.

This creates a split screen. While we are still seeing many companies “hold the line” with elevated valuations, everyone knows that much of this is illusory.

This is precisely the reason so many funds also have a huge amount of dry powder. A few partners at well-known funds have mentioned to me that while they are trying to invest in high-flying AI names, their funds are also reserving a significant portion of capital to support existing companies.

Part of this is good. We, ourselves, said to our LPs during our last Summit/AGM, “We’re all special situation funds now,” referring to the many disruptions presented by a market in crisis. Many of these cases do not have happy endings. However, others are once-in-a-blue-moon opportunities. In our most successful case, we re-upped on a company whose valuation plummeted to a fraction of its 2021 high (5X’ing our share of the preferred), where most investors have been wiped out, but the company itself has had exponentially growing revenue and whose new valuation barely exceeded a 2X revenue multiple.

That’s a good case for reserving capital. The bad case—which, unfortunately, is much of the market—is to keep your existing companies from collapsing in valuation.

Marks tell the story

How do we know that most of the market is “the bad case”? Other than anecdotal chatter, we see it in most funds’ marks on their companies. Many of these marks are still extraordinarily elevated, even in companies that we know behind the scenes are distressed.

We’ve heard it in cases where we’ve aggressively marked down our companies and been asked why since a similar (or even the same) company has not been marked down by other funds.

We like our portfolio. We think many will become world-changing companies. We also think that it’s insane to assume that company valuations should look like they did in 2021. Private capital supply and demand have drastically changed. Additionally, while US public markets are historically elevated (the forward earnings risk premium is negative for the first time in a long time), a lot of it is driven by a tiny number of mega-companies, and both IPOs and M&As are still sluggish.

This isn’t self-congratulatory patting ourselves on the back about how honest we are. In truth, it’s quite painful to have supposed apples-to-apples performance metrics (spoiler: they never are) that look worse than our peers, but we think it’s important in both keeping the trust of our LPs and us sleeping well at night. As Sarah Samuels stated in the Institutional Investor article, the current dynamics have been destroying a lot of goodwill between GPs and LPs.

However, even besides that, we think inaccurate valuations are extremely unhealthy for the industry.

Inaccurate valuations freeze markets

As many know, James came from Bridgewater’s investment team and has a global macro and public markets background. One lesser-known aspect of Bridgewater’s culture—driven by Ray—is that they tend to be market history nerds. James, in particular, has been fascinated by Japan’s Lost Decade(s) for many years. (One accessible book recommendation from him is “The Holy Grail of Macroeconomics: Lesson from Japan’s Great Recession” by Richard Koos.)

Why did Japan suffer sluggish growth and deflation for so long? A big part was valuations—specifically, for assets on the banking sector’s books—were frozen in amber.

Rather than face the prospect of a messy and potentially catastrophic financial sector collapse, Japan allowed their banks to simply ignore reality. They may be insolvent in reality, but if simply no one recognizes it, life goes on.

Well, kind of. The problem is, that no one is actually fooled, even if everyone is willing to pretend that the emperor has no clothes. Banks know that they can’t afford to take even more losses, which means that they’re unwilling to issue risky loans. This means—in Ray’s framework that growth is driven by money and credit—that credit is severely curtailed, which cycles back to generate less total money in the economy (because one person’s spending, whether from money or credit, is another’s revenue). Combined with a conservative central bank that was never really comfortable easing further out on the risk/duration curve, this was a disaster. It meant Japan barely limped along until a combination of literal decades (slowly growing out of the debt hole) and a push from Abenomics finally got them out.

Today, while they’re starting to get out of it, China has faced a similar problem in their regional governments, SOEs, and shadow banking sector.

And famously, the US avoided Japan’s fate in the aftermath of 2008 by aggressively recognizing and forcing consolidation of weak banks and going out with “Bazookas of cash” from fiscal policy and monetary policy far out on the risk/duration curve (Quantitative Easing). Essentially, the opposite of everything Japan did.

Lessons for today’s VC and PE market (from James)

Mid-last year (2024), I had dinner with a group of VCs. No one thought the fundraising (for either funds or startups) was great.

After hearing about my background and deep skepticism about substantial rate cuts—since inflation and growth conditions did not warrant it—I was asked what, I thought, would drive an unfreezing of the venture market. Specifically, I got a particularly thoughtful question from one particular VC that I respect a lot. She asked, “Sure, time will eventually fix the market. But what’s a realistic scenario that would cause it to actually rapidly improve?”

It took me a bit of thought.

And then my answer horrified the table.

“Mass collapse of late-stage startup valuations, with forced recognition of existing losses, and then forced consolidation or fire-sale of the companies.” The table didn’t really like the answer. One GP mentioned that that would damage the venture industry’s reputation and prospects for a generation. Another grumbled that even if that worked, all of our businesses would be dead.

However, the question-asker was more considered. She asked, “Why?”

It took me a while to clarify at the dinner, but you, dear reader, probably can already see why after the explanation about Japan.

The venture market is frozen because commitments are high, distributions are low, and without the willingness to recognize losses, nothing transacts (despite the vaunted statements by secondary firms about how much business is getting done).

If losses were recognized—and allowed to be realized—distributions, even if disappointing, would actually happen, firms would no longer be sitting on as much capital to support existing companies (and would probably desperately seek fresh, exciting opportunities… to dig themselves out of the hole) and the entire cycle of commitments, capital calls, and distribution would be unfrozen.

What it would take is recognizing reality. History teaches us it’s better to rebuild back from the ground up rather than fall from grace on a shaky, unstable foundation.

Final thoughts

There is a (perhaps niche) saying in hedge funds that you can’t “eat” simulated, gross, or paper returns. The idea is that these metrics of theoretical money are not going to pay for your lunch.

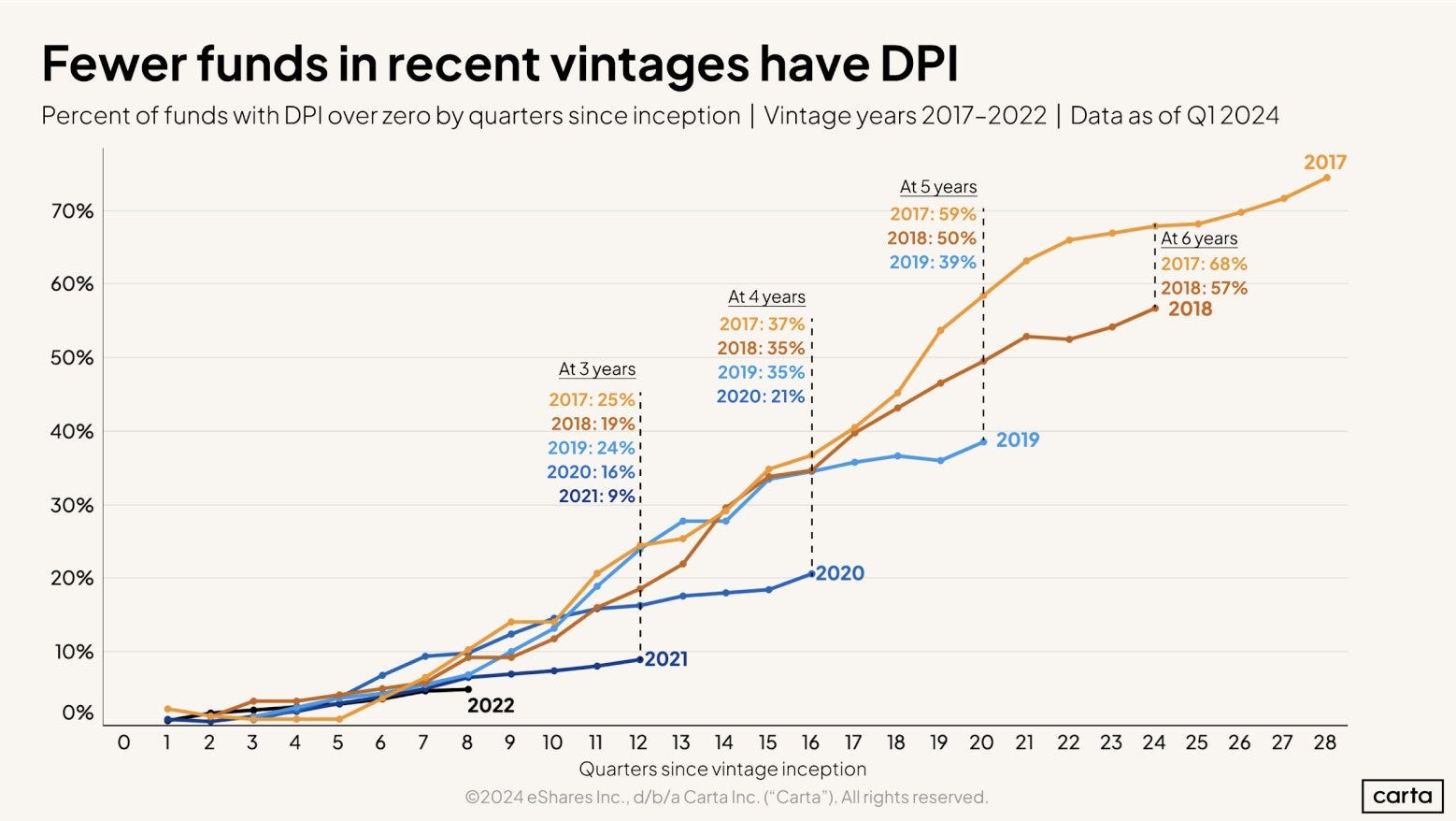

Similarly, one can’t eat TVPI. You can only actually eat DPI, which is low across the board for venture funds right now.

Venture capital already, famously, has a painfully low correlation between interim performance (TVPI or DPI) and final DPI. David Clark of VenCap analyzed 71 funds from 2005-2008—the correlation between year 5 TVPI/DPI and final TVPI/DPI was 0.4 and 0.2 respectively. Worse, some of the best/worst performers at t=5 years flipped at t=15 to 20 years.

Beezer Clarkson from Sapphire Partners noted similarly that in their venture portfolio, funds get to 1X DPI by year 8 on average. And many of their best performers returned absolutely nothing by year 5 (even in better liquidity environments than today).

So, does this mean one just has to throw up one’s hands and accept that there’s no way to assess venture capital? No, but it does mean that the job comes back to whether you think the VC’s strategy makes sense, if they can execute, and if you trust them.

VC is always weird because the time scales mean that we always have to raise sooner than we know the “final results” of our funds. However, as one of our advisors has constantly emphasized to us, the entire ballgame is about getting (more) money back to your LPs. So long as you try to do that, things will work out—or, at the very least, you can know that you did right by those who trusted you.

In other news

Portfolio News

As per Axios Pro:

Terra plans to use the funds to build its first commercial plant in Cleburne, Texas, that can make a quarter of a million tons per year of its supplementary cementitious material to be blended to produce low-carbon cement. Terra has pre-sold that first plant to Asher Materials, a subsidiary of NSG Logistics.

Catch us in person!

James will be moderating an all-star panel on the future of AI at SXSW on March 8th. Panelists include:

Sergei Polevikov, writer of AI Health Uncut, founder of WellAI, and a Ph.D.-trained data scientist, AI entrepreneur, economist, and quant investor with over 30 academic manuscripts.

Kartik Tiwari, a roboticist and a three-time founder of companies working on hard problems from self-driving trucks (Starsky Robotics) to autonomous robotic surgery (Andromeda Surgical).

Chidi Nwankpa, a Principal at Gore Range Capital (and previously a summer associate and venture partner at Creative!), co-founder of GlobalHealth AI, and holds both an MD (University of Benin) and an MBA (University of Chicago Booth).